In his new book Smart People Should Build Things, the founder of Venture of America Andrew Yang offers up advice on how aspiring entrepreneurs can begin getting their startup dream off the ground.

Source : http://www.entrepreneur.com/article/231130

Showing posts with label entrepreneur. Show all posts

Showing posts with label entrepreneur. Show all posts

Wednesday, October 01, 2014

Common Characteristics of Entrepreneur

Some 25 common characteristics you can find on Entrepreneurs

Full article at : http://www.entrepreneur.com/article/200730

Full article at : http://www.entrepreneur.com/article/200730

Tuesday, September 30, 2014

Tuesday, July 22, 2014

Eureka moments

A man couldn't fit a table in his car. He took off the legs and said, "Aha!" He founded Ikea.

These are their stories. The story of entrepreneurship moments.

Thursday, July 03, 2014

Young Entrepreneurs: Under 30 and On Fire

Young Entrepreneurs: Under 30 and On Fire

Stanford UniversityLOCATION:

Cemex Auditorium | Stanford University

655 Knight Way

Stanford, CA

Tuesday, January 21, 2014

VLAB is back with one of the most anticipated events of the year: Young Entrepreneurs - Under 30 and On Fire. We are tapping into the minds of some of the most successful innovators under 30 in the heart of Silicon Valley. They are doing it all: raising money, leading talented teams and steering their vision forward.

Five young entrepreneurs, all under the age of 30 will share their stories as they inspire us with the power of their ideas and their relentless passion to execute.

Moderated by Adam Draper, CEO and Founder of Boost Incubator, our panel will feature:

Michael Carter, CEO at Game Closure, raised $12M to tackle the hardest problems in mobile gaming and is recognized by W3C for his initial design of the HTML5 WebSocket real-time technology that is used in all modern web browsers

Melody McCloskey, CEO at StyleSeat, a woman entrepreneur recognized in 2010 by Business Insider as a Silicon Valley 100

James Tamplin, CEO & Co-Founder at Firebase, a co-founder of a realtime application platform that allows developers to synchronize data instantaneously

Lat Ware, Founder at Crooked Tree Studios, a game developer who successfully launched a game with telekinesis like powers on Kickstarter

Marcus Weller, Ph.D., CEO & Chairman of Skully Helmets, the CEO of a heads-up display motorcycle helmet which won the coveted DEMO God award at their 2013 launch

Legendary investor Tim Draper

Some of the superstar companies that are ventured and funded by Tim Draper:

- Tesla

- Skype

- Path

- Box

- Baidu (China's Google)

- and others (400 companies)

Even have his own Draper University of Heroes.

Thursday, May 29, 2014

Business books

Business books I want to own

If you want to bone up on your business theory, here are the central lessons — and a great way to begin a reading list.

http://www.businessinsider.my/famous-business-book-summaries-2014-5/

If you want to bone up on your business theory, here are the central lessons — and a great way to begin a reading list.

http://www.businessinsider.my/famous-business-book-summaries-2014-5/

Quiz Week 4

Question 6

Discuss common pitfalls that entrepreneurs experience in

selecting which ideas to develop into new ventures. Please respond in one

paragraph.

Answer for Question 6

Successful entrepreneurs introduce a product or service that

satisfies customer needs in a better way than competitors, and at a price that

is greater than the cost of creating and delivering that product or service. To

understand how to fulfill customer needs at an attractive price, four areas are

critical to assess: macroeconomic changes, industry conditions, industry

status, and competition. As a first step to exploring new venture ideas, search

for sources of pain or aggravation for customers, as these are prime

opportunities for new products. The best clue that a new product or service is

needed, are customer complaints about existing products and services.

Question 7

Discuss four types of macro changes that increase new

venture opportunities. Please respond in one to two paragraphs.

Answer for Question 7

Types of changes that increase new venture opportunities

includes changes in technology, changes in social and demographic factors,

changes in political and regulatory rules. Technical change is one of the most

important triggers of change, because new technology allows for the expansion

of new innovations. The magnitude of technical change is important. Significant

change can create entirely new markets. The larger the technical change, the

greater the opportunity for new businesses to be created. Societal change opens

up opportunities for new businesses by altering people’s preferences and

creating demand for things where demand had not existed before.

Demographic changes can create a host of entrepreneurial

opportunities. Each trend offers new opportunities for products and services to

serve these customers. Political changes can introduce opportunities or

challenges for entrepreneurial ventures. It is valuable to consider how local, state,

or national government decisions may change policies. These can challenge

existing companies, and open new opportunities for new companies. This type of

change creates opportunities because it is productivity enhancing. In other

cases, changes generated are not productive, but merely shifts value from one

set of economic factors to another.

Question 8

What questions should you consider in determining how to

produce the product for your venture? Please write three questions.

Answer for Question 8

What is the best way to assess customer needs?

Why does my product fit customer needs better than those of

current and future competitors?

What price should I charge?

Question 9

What demographic and psychographic changes are creating new

market needs in business areas that interest you? Please respond in one

paragraph.

Answer for Question 9

Demographic changes can create a host of entrepreneurial

opportunities. Each trend offers new opportunities for products and services to

serve these customers. Some that interest me are assisted living centers for

the elderly, foreign language radio, and organic food stores. While

psychographic change examines shifts in attitudes, values, opinions, interests,

and related personal factors of markets. These are contrasted with demographic

variables in that psychographics involve how people think and feel.

Question 10

What technical advancements, political changes, and/or

regulatory changes are creating new market opportunities in business areas that

interest you? Please respond in one paragraph.

Technical changes are one of the most important triggers of

change, because new technology allows for the expansion of new innovations. For

example, invention of portable cassette players leads to portable compact discs

players which leads to the development of portable MP3 players and then leads

to the capability to play songs on mobile phones. Political changes can

introduce opportunities or challenges for entrepreneurial ventures. It is valuable

to consider how local, state, or national government decisions may change

policies. These can challenge existing companies, and open new opportunities

for new companies. I am being aware of the political shifts that will influence

business policy, taxation, corporate social responsibility, environmental

issues, or consumer protection with my venture. Governmental regulations affect entrepreneurial

ventures in a variety of ways. Managerial regulations govern what the owners

and operators of companies can and cannot do. Technology regulations influence

standards, interoperability, safety, and a host of related areas. Price

regulations often dictate pricing strategies that support fair competition,

which along with competitive regulations, are designed to protect consumer interests.

Saturday, May 24, 2014

Grow to Greatness

I want to take this course, but it is not available for the time being.

https://www.coursera.org/course/growtogreatness

Grow to Greatness: Smart Growth for Private Businesses, Part I

This course focuses on the common growth challenges faced by existing private businesses when they attempt to grow substantially.

Most entrepreneurship courses focus on how to start a business. Few focus on the next big entrepreneurial inflection point: how do you successfully grow an existing private business? This is the focus of this Course. It is based on the instructor's research and thirty years of real-world experience advising private growth companies.

This Course will challenge how you think about growth; give you tools to help you plan for growth, assess the preconditions to grow, and manage the risks of growth. You will study stories of how five different private businesses faced their growth challenges.

Growth, if not properly managed, can overwhelm a business, destroying value and in many cases even causing the business to fail. However, the research shows that every growth business faces common challenges. You can learn from others' experience—you do not have to "reinvent the wheel".

The Course format is case based. Each case tells a compelling story. You will learn from Julie Allinson, Susan Fellers, Dave Lindsey, Parik Laxinarayan and Eric Barger. In addition, each week, we will discuss a different content theme. In Weeks and 2 and 5, you will engage in Workshops where you will be asked to use and apply the Course tools and concepts to create growth strategies for two different real-life businesses. You will have the opportunity to create a Course Community of fellow-students to learn from each other as the Course progresses.

You will learn about the: "3 Myths of Growth"; the "Truth About Growth"; why growth is like "Mother Nature"; the "Gas Pedal" approach to growth; the all important "4 Ps" of how to grow; and how to scale a business strategically.

Week 1: The "Truth About Growth":The common beliefs that all growth is good; bigger is always better; and businesses must "grow or die" are not true. Growth can be good and growth can be bad. There is no scientific basis for the axiom "grow or die". It is a fiction. You will lean from Julie Allinson, the founder of Eyebobs, who has built a successful business selling stylish “reading glasses for the irreverent and slightly jaded.” Julie approached growth realistically and understood its value creation and destructive powers. You will learn how she faced manufacturing, sales, and people challenges while building a high growth business—a cool story.

Week 2: Workshop—“Are You Ready for Growth?”: Using the Growth Risks Assessment Tool from Week 1, you will meet and advise Susan Fellers, the founder of 3 Fellers Bakery. Susan started a business baking gluten-free products when she was diagnosed with celiac disease. Her start-up was successful, and she needs your help because she has had so many growth alternatives and she does not know which to pursue. You will be asked to create a growth plan for her.

Week 3: The 4 Ps of Growth—Planning, Prioritization, Processes and Pace:Using the Defender Direct story, we will learn to better manage the chaos of growth; find a business's strategic focus; how to choose which daily "fires" to put out first; how to create replicable processes—“leave a fire extinguisher behind"; and how to pace growth letting "up on the growth gas pedal". Dave Lindsey is our business builder this week, and you will trace his story from starting his business in his home to today being a national, privately owned home installation company generating well in excess of $300M (USD) in revenue with healthy profit numbers.

Week 4: The Four Ways To Grow a Business: This week you will learn about the different ways to grow—improvements, innovation, scaling, and strategic acquisitions—with a focus on growth boosters: how to get more customers and sell more products and/or services to existing customers more efficiently. Enchanting Travels, a travel company based in India, is our story this week. You will learn how they built the foundation of their business to scale their focused customer value proposition so they could grow geographically to Africa, South America, and Asia. The story presents a big decision for you: should they franchise their business?

Week 5: Workshop—“Creating a Growth Plan": This week you will read about Eric Barger's challenge: how to take a business that has had little growth selling a commodity product and turn it into a high growth business. You will be asked to create a growth plan for Eric. And after doing that you will learn what Eric did to quadruple his business in three years.

The 1 percent

Here are four things the 1% do, that you are not willing to and the reason why you will always stay part of the 99%.

They take chances on themselves, they always have.

While most people think of starting a business or bringing an idea to life as a risk, the 1% thinks not doing anything about it is the actual risk, not the failure associated with trying. You have to understand that there is no such thing as a golden idea, and that finding a special idea is not more likely to succeed than the next. You, and you alone, are the reason your idea will come to life and flourish or be killed by your audience. The chance you are taking is not on the idea but rather that you believe in yourself enough to see it through to the end. When I, myself, started Secret Entourage, the idea behind the movement was not a genius one, nor was it one that I was best fitted for since I knew nothing about the internet, but it was founded solely on the belief that regardless of how many times we failed, we would continue forward until we do. If you have followed us since day 1, then you are very familiar with how many times we changed and revamped Secret Entourage for it to become what it is currently. It wasn’t born out of genius, it was born out of belief and perspiration.

They don’t have ideas, they work on their plans.

While most of the 99% has or had a great idea at some point in their life, the 1% isn’t worried about sharing with the world their geniusness for coming up with an idea. As a matter of fact, you may not even know they are working on something or that they are the owners behind a brand or website until it starts to become very popular. Creating powerful plans and executing is why they are more likely to succeed from the 1% who shares their vision of what they could have or could have had since their great idea. The real difference is that their ideas are great stories to tell others, rather than a plan that is being worked on.

They are not worried about what others have done, are doing or what others think.

The 99% always needs re-enforcement and motivation to keep going, and even need to be reminded as to why they are the ones that will succeed. The 1% doesn’t worry about self-recognition or peer pressure, regardless that it is positive or negative. Think about competition, and its impact on the 99%. While many would think the Five Guys franchise is a competitor to McDonalds, the founder of Five Guys never believed it to be and went ahead and started anyways. The difference lies in the belief, rather than the excuse. If you believe your brand enough, then you understand there is no competition to it on any level and you alone are your greatest competitor. The 99% gauge the possibilities based on what others have done, the 1% create possibilities based on their own belief.

They understand the difference between having resources and being resourceful.

While the 99% complain about not having enough capital to start or gain traction, the 1% finds a way with or without resources. You may be surprised to know that when you actually make a considerable amount of money, you are more cautious of spending it and many of today’s new businesses are founded on resources outside of money, before being injected with money. The excuse is not valid, it is a simply a deterrent the 99% use to never get started.

Being part of the 1% requires you to do more than just understand the basics that makes us successful. It requires you to become a doer, a believer and very aware person, all of which are in your hands and not tied to having enough money or obligations. At the end of the day, you are the reason why you will never join the 1%

Sunday, May 18, 2014

Quiz Week 2

I have to submit these today. I'm taking Developing Innovative Ideas for New Companies: The First Step in Entrepreneurship by Dr. James V. Green

Entrepreneurs assess real risk and improve decision-making by

using the following keys. They apply multiple perspectives to a decision situation,

they integrate these perspectives into the decision, they use a complex

cognitive framework regarding a decision situation, and they have broader and

deeper view of the decision at hand which may result in a more accurate assessment

of risk.

Update: I got a score of 10.38 out of 12.00

Question 5

How would you define the "entrepreneurial

mindset"? Be sure to discuss each of the five factors. Please respond in

one to two paragraphs.

Entrepreneurial mindset has five factors. They are; high

need for achievement, individualism, locus of control focus, and optimism. Need

for achievement is defined as having a preference for challenge, an acceptance

of personal responsibility for outcomes, and a personal drive for

accomplishment. Individualism means that entrepreneurs need less support or

approval from others. High individualism is associated with an emphasis on individual

initiative and achievement. Often results in entrepreneurs needing less support

or approval from others.

Control has two segments, which is autonomy and locus of

control. Autonomy is an individual’s belief about their level of freedom from the

influence of others. Locus of control is an individual’s belief that they can

influence the environment in which they are found. People with higher levels of

autonomy and an internal locus on control are more likely to discover an

entrepreneurial opportunity. Internally-oriented locus of control people

believed that they are able to influence their environment.

Successful entrepreneurs are able to focus attention on a

single task and see it through to completion. This leads selected individuals

to react and to become successful entrepreneurs. While optimism enables

entrepreneurs to try new things and attempt difficult tasks, optimism may also

present negative impacts. Optimism leads entrepreneurs to frequently make judgements

on subjective positive factors.

Question 6

We are interested in your personal perspectives on

"entrepreneurial motivation". Discuss each of the three factors

through which goal-directed behavior is initiated, energized and maintained as

related to entrepreneurial strategic decision-making. Please respond in one to

two paragraphs.

Entrepreneurial motivation is having high self-efficacy in

all task, having high cognitive motivation, Self-efficacy is defined as one’s

belief in one’s ability to accomplish a specific task. Self-efficacy differs as

it is task dependent. For example my self-efficacy is low in selling in an

audience because I fear public speaking. In improving one’s self-efficacy,

there different approaches, namely; increasing mastery, having a role model/observing,

verbal encouragement from trusted sources like a coach or mentor, and exhibiting

a positive mood and high energy.

Cognition is the process of thought. Individuals exhibiting

a high need for cognition tend to seek, acquire, think, and reflect on relevant

information. In other words their brain is active in thinking for solutions all

the time. Tolerance for ambiguity is defined as the tendency to perceive ambiguous

situations as desirable rather than threatening. Entrepreneurs make complex decisions

in ambiguous situations and desire them. It is a necessary factor for

entrepreneurs based on dynamic nature of markets and competition.

Question 7

In considering the role of "risk" in entrepreneurial

decision-making, why do entrepreneurs accept risks that traditional managers

may avoid? Please respond in one paragraph.

Entrepreneurs engage in risk that traditional managers may

avoid because they have intuition, have individualistic view, have high

tolerance for ambiguity and high confidence in skills, knowledge, and expertise.

Entrepreneurs mitigate risk based on intuition which is improved through past

experiences. They have individualistic view complemented by relationships and

team orientation. They have high tolerance for ambiguity based on comfort with

making difficult choices with in complement information in the past. And lastly

they have high confidence in skills, knowledge, and expertise enhanced based on

past success.

Entrepreneurs engage in risk that traditional managers may

avoid because they lack in necessary information in a situation needing prompt

decision. They develop an inside view of the decisions they face. They also ignore

elements of past situations. And they favor positive possible outcomes over

negative outcomes. Entrepreneurs assess real risk and improve decision-making by

using the following keys. They apply multiple perspectives to a decision situation,

they integrate these perspectives into the decision, they use a complex

cognitive framework regarding a decision situation, and they have broader and

deeper view of the decision at hand which may result in a more accurate assessment

of risk.

Question 8

How can you improve your confidence level and risk

tolerance? Please respond in one paragraph.

Entrepreneurs need to improve their confidence level and

risk tolerance. It is important for entrepreneurs to believe in themselves and

their abilities, balanced by the reality of the tasks at hand. It may require them

to go against the norm, and against popular opinion and advice of friends and

family. They need to address their self-doubts. Entrepreneurs also need to addresses

their willingness to accept risk, perceive risk differently, consider the

risk-reward balance, and their potential to return to the status quo.

Question 9

How can you increase your comfort level with making

strategic decisions quickly, with limited information and high consequences?

Please respond in one paragraph.

Update: I got a score of 10.38 out of 12.00

Tuesday, April 29, 2014

Superentrepreneur

Wow now there are superentrepreneur.

"SuperEntrepreneurs" are the Cinderellas of the business world. They're the most entrepreneurial of entrepreneurs, the extreme rags to riches stories: they are self-made billionaires.

Self-Made Billionaires Around the Globe: Where and Why They Thrive (Infographic)

"SuperEntrepreneurs" are the Cinderellas of the business world. They're the most entrepreneurial of entrepreneurs, the extreme rags to riches stories: they are self-made billionaires.

Self-Made Billionaires Around the Globe: Where and Why They Thrive (Infographic)

Will I Succeed?

Most likely yes. If you're a veteran and 30% of what you do will have success in them. I think.

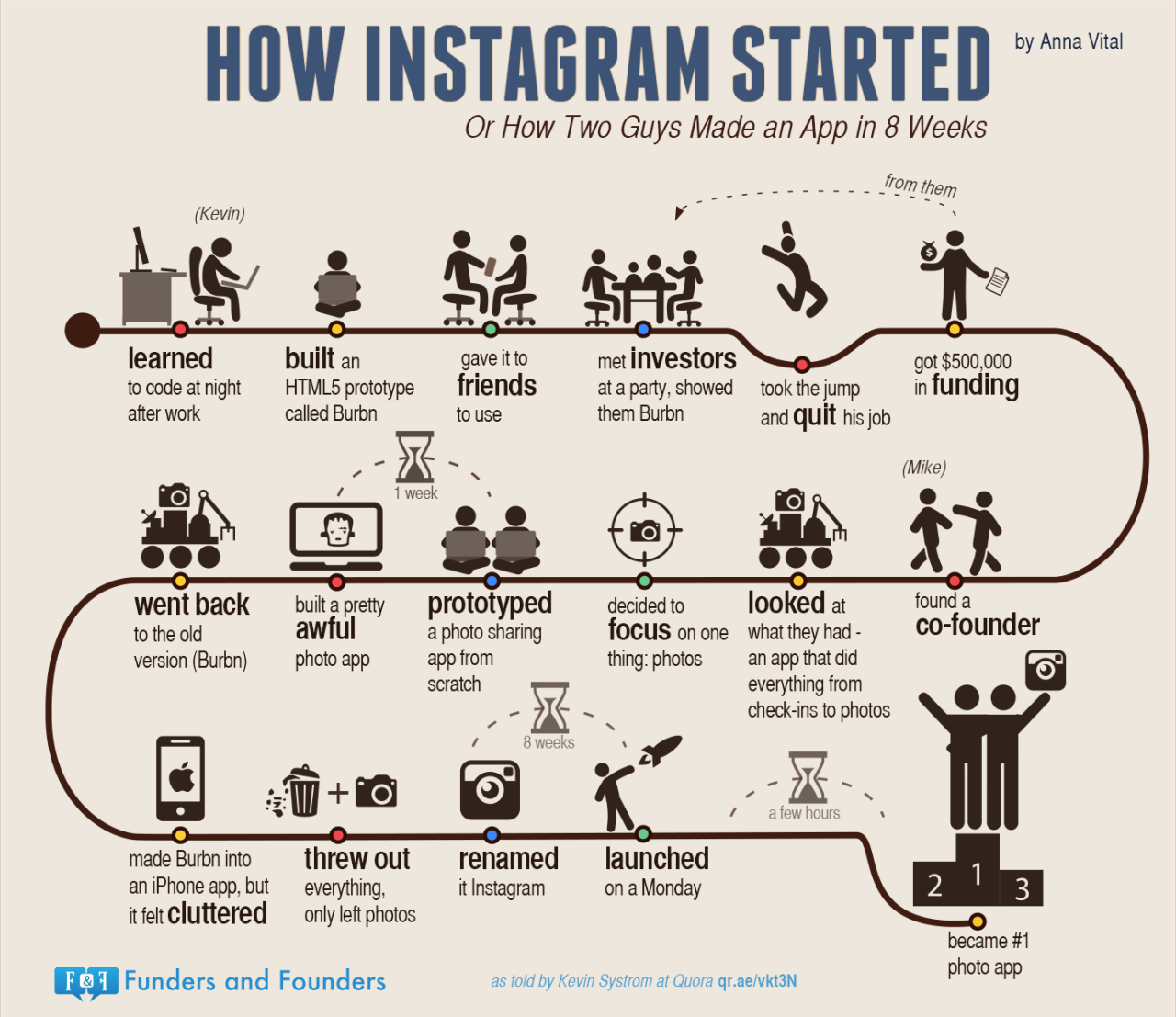

Source : http://fundersandfounders.com/will-i-succeed-with-my-startup-the-odds-of-making-it/

Source : http://fundersandfounders.com/will-i-succeed-with-my-startup-the-odds-of-making-it/

Wednesday, April 16, 2014

Leading impactful life

I should be doing this. Right, now I have to find 1000 people to try the product and grow from there.

http://fundersandfounders.com/counting-the-people-you-impact/

http://fundersandfounders.com/counting-the-people-you-impact/

Tuesday, April 15, 2014

Entrepreneur

Well then, I might be not entrepreneur material

- You come from a family of individuals who just couldn't work for someone else. Your parents worked for themselves. Though this isn't true for every entrepreneur (myself included), many have a family history with one or both parents having been self-employed.

- You hate the status quo. You’re a person who is always questioning why people do the things they do. You strive to make things better and are willing to take action on it.

- You’re self-confident. Have you ever met an entrepreneur who was pessimistic or self-loathing? After all, if you don’t have confidence, how can others believe in you? Most entrepreneurs are very optimistic about everything around them.

Monday, April 14, 2014

Friday, April 11, 2014

Creativity

Originally I was about to save this video to my hard drive, but I couldn't and I don't know how to.

Need some motivation or inspiration to finish a project? Here are 29 ways to keep you going!

Habits of Entrepreneurs

What are habits of entrepreneurs that some people don't have any?

I found some on Quora

- Most people spend their money to get the most utility - fun, food, whatever. Entrepreneurs spend their money to make the most money. This one habit pretty much accounts for everything, and it's a big reason why the rich get richer, and the poor stay poor.

- Time and attention conscious. Time and our attention are the only truly finite constraints - incalculably precious and easily squandered. Successful entrepreneurs are absurdly conscious of the fact, and tend to become highly organised, intolerant of inefficiency and laser focused. Many famous figures famously wear the same outfit every day (Zuckerberg, Jobs) claiming that anything else is an unnecessary waste of their attention.

- Develop skills that compound. Entrepreneurs even think of their own skills as an investment; whatever time they put in should have the greatest possible return. For example: creating software, leading others, spotting future trends. They are typically self-taught, and diligently so. They work to make themselves the type of person who would be wealthy.

- Constructive attitude. True entrepreneurs look for ways to make ideas work, while regular people focus on why they won't work. If entrepreneurs hit an obstacle, they mobilize and seek ways to overcome it. Regular people see it as an excuse to give up.

- Focus on Value. Entrepreneurs understand the idea of value. Whatever they do, they make sure the value created is larger than the cost of resources used. Regular people tend to focus on expenses. Remember those driving around parking lots for 30 minutes just to save 5 minutes of walking?

- Sense of Urgency. Successful entrepreneurs are usually out of time. Presented with a task, they seek the most efficient, fastest path to complete it and move on, keeping an eye on a big picture. Regular people tend to dwell on minor details and get stuck in the woods.

- Crossing the tightrope without a net. This is not to say successful entrepreneurs don't perceive risk, or that they take inordinate amounts of risk. Or that they don't worry all the time they won't make payroll, or will fail, or not make it. Not at all. They see all of this. In fact, in my experience at least, they are highly risk averse where they see risk they cannot overcome.

- They get shit done. They don't just come up with ideas and tell their friends and then slowly forget about them. They execute.

- They don't have a problem with uncertainty. What kind of health insurance will I have? What if the competition just copies my idea? How will I raise money? What if somebody already has a patent for this? These kinds of unanswered questions would cause most people not to create Facebook even if they were given a time machine and flown back to 2003. They don't bother successful entrepreneurs. They have confidence they'll be able to figure things out and they are at peace with the fact that what they are doing is inherently risky.

Subscribe to:

Posts (Atom)